Strategies for Scaling Fintech Startups Across Africa

Introduction: Scaling in Africa Is Not Linear

Scaling a fintech startup in Africa is not just about growth—it’s about navigation. Unlike more uniform markets, Africa is a multi-layered ecosystem of 50+ regulatory environments, fragmented payment rails, diverse consumer behaviors, and infrastructure gaps.

What works in Nigeria may fail in Kenya. What scales in South Africa might stall in Francophone West Africa.

This is why many fintech startups don’t fail because of poor product-market fit but because they underestimate operational complexity.

The companies that win are not just quick; they are structurally prepared to scale.

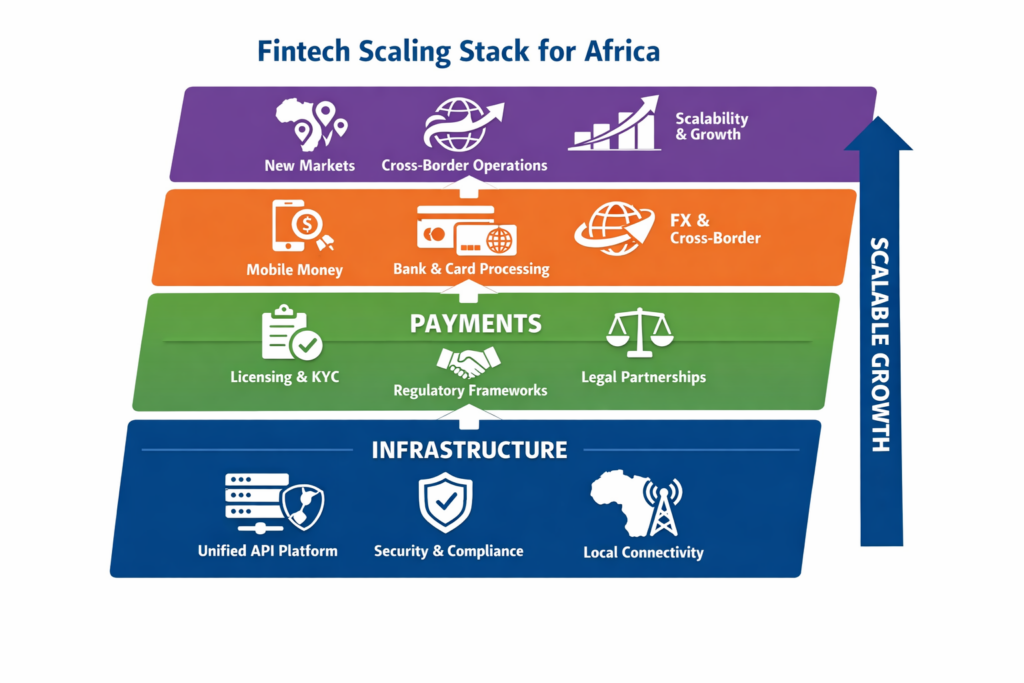

1. Build for Fragmentation, Not Uniformity

Africa is not one market. It’s a network of distinct economies.

Key realities:

- Payment methods vary dramatically (mobile money vs cards vs bank transfers)

- Currency volatility impacts pricing and settlement

- Infrastructure maturity differs across regions

What this means in practice:

Instead of building one system and adapting later, design a modular architecture from day one.

Winning approach:

- API-first infrastructure

- Plug-and-play integrations per market

- Localized UX (languages, flows, trust signals)

Platforms like Unipesa enable this by offering a unified API layer across multiple payment methods and countries, reducing the need for market-by-market rebuilds.

2. Treat Compliance as a Growth Lever, Not a Barrier

In Africa, regulation serves as a competitive moat rather than a source of friction.

Each market has:

- Licensing requirements

- KYC/AML frameworks

- Data residency rules

- FX controls

The mistake:

Startups delay compliance until expansion, which blocks growth.

The winning strategy:

- Build compliance-by-design systems

- Partner with infrastructure providers that already support regulatory frameworks

- Engage local legal expertise early

Companies that scale successfully treat compliance as part of the product, not a backend obligation.

3. Localize Payment Acceptance to Increase Conversion

One of the biggest scaling mistakes is assuming global payment methods will work locally.

They won’t.

Reality:

- In East Africa → mobile money dominates

- In Nigeria → bank transfers and wallets are critical

- In North Africa → cards are more common

Impact:

Poor localization = lower conversion rates + higher transaction failures

Strategy:

- Integrate locally preferred payment methods

- Enable smart routing and fallback mechanisms

- Optimize checkout flows per region

With infrastructure platforms like Unipesa, fintechs can:

- Access mobile money, banks, and cards through one integration

- Implement routing logic without building it from scratch

4. Solve Cross-Border Complexity Early

Cross-border payments are one of the biggest opportunities—and challenges—in African fintech.

Challenges include:

- Currency conversion inefficiencies

- Settlement delays

- Regulatory barriers

- Limited interoperability between markets

What scaling startups do differently:

- Build cross-border capabilities from the beginning

- Use infrastructure that supports multi-currency processing

- Optimize FX handling and settlement flows

Instead of treating cross-border as an “expansion phase,” treat it as a core capability.

5. Focus on Unit Economics Before Geographic Expansion

Scaling across Africa can quickly become expensive:

- Licensing costs

- Local partnerships

- Infrastructure adaptation

- Operational overhead

The trap:

Expanding into multiple countries too early → burning capital without profitability

The smarter path:

- Achieve strong unit economics in 1–2 core markets

- Validate your model

- Then replicate with infrastructure support

Scaling is not about being everywhere—it’s about being efficient where you are first.

6. Build Strategic Partnerships, Not Just Integrations

Fintech scaling in Africa is ecosystem-driven.

You need:

- Banks

- Mobile network operators

- Payment aggregators

- Regulators

- Local distributors

The shift:

From transactional partnerships → to strategic alliances

Example:

Instead of integrating with multiple providers independently, startups leverage platforms like Unipesa to:

- Access pre-integrated networks

- Reduce time-to-market

- Simplify operational complexity

Partnership strategy becomes a growth accelerator, not a bottleneck.

7. Invest in Infrastructure, Not Just Frontend Experience

Many startups over-invest in:

- UI/UX

- Branding

- Customer acquisition

…and under-invest in:

- Payment reliability

- Transaction success rates

- Backend scalability

The truth:

In fintech, infrastructure is the product.

If payments fail:

- Users churn

- Merchants lose trust

- Growth stalls

Priority shift:

- Ensure high transaction success rates

- Implement redundancy (fallback routing)

- Monitor performance across markets

This is where infrastructure-first platforms like Unipesa provide a critical edge.

8. Use Data to Drive Expansion Decisions

Scaling decisions should not be instinct-driven—they should be data-driven.

Key metrics:

- Transaction success rates per country

- Cost per transaction

- Customer acquisition cost (CAC)

- Retention rates

- Payment method performance

Smart scaling approach:

- Expand where your data shows natural traction

- Optimize before entering new markets

- Continuously refine based on performance

9. Build Trust Through Reliability and Transparency

Trust is one of the biggest barriers in African fintech.

Users care about:

- Transaction reliability

- Transparency in fees

- Speed of settlement

- Customer support

Scaling insight:

Trust compounds growth.

Startups that win:

- Communicate clearly

- Deliver consistent performance

- Resolve issues quickly

Infrastructure reliability directly impacts brand perception.

10. Move from Startup to System

The final shift in scaling is organizational, not just technical.

Early-stage fintechs operate like products.

Scaled fintechs operate like systems.

This means:

- Standardized processes

- Scalable infrastructure

- Regional operational models

- Strong governance frameworks

Companies that succeed across Africa evolve from:

“a fintech app” → to → a financial system layer

Conclusion: Scaling Requires Infrastructure Thinking

Scaling fintech across Africa is not about moving faster—it’s about building smarter.

The winners are:

- Infrastructure-first

- Compliance-ready

- Locally adapted

- Data-driven

Platforms like Unipesa play a key role in enabling this shift—helping startups move from fragmented builds to scalable, unified systems.