From Retail Shops to Agent Networks: Versatile Use Cases for Unipesa’s POS System

Introduction: POS Systems Are No Longer Just Payment Devices

For years, POS terminals were viewed as simple transaction tools.

Their role was straightforward:

- accept payments

- process transactions

- print receipts

Today, that role has changed dramatically.

Modern POS systems are becoming:

multi-functional financial infrastructure layers

They support:

- retail commerce

- agent banking

- cash-in and cash-out operations

- wallet services

- bill payments

- SME financial services

And in emerging markets, where financial systems are highly dynamic, POS infrastructure is evolving into one of the most important components of digital finance.

This is where Unipesa positions itself—not simply as a POS provider, but as an infrastructure platform capable of supporting diverse transaction ecosystems.

The Evolution of POS Infrastructure

Traditional POS systems focused mainly on:

- card acceptance

- merchant transactions

Modern systems operate very differently.

They are designed to:

- connect multiple payment rails

- support different transaction types

- function across diverse operational environments

Key shift: POS systems are moving from transaction devices → to infrastructure nodes.

Why Versatility Matters in Emerging Markets

Financial environments across emerging markets are fragmented.

Different users rely on:

- cash

- mobile wallets

- bank transfers

- merchant payments

- agent-assisted transactions

A rigid payment system cannot efficiently serve all of these needs.

Businesses require flexibility.

They need systems capable of operating across:

- retail environments

- informal commerce

- financial service points

- distributed agent networks

Retail Shops: Beyond Basic Transactions

One of the most common POS use cases remains retail commerce.

Retail businesses use POS systems to:

- accept digital payments

- manage checkout flows

- improve customer convenience

But expectations have evolved.

Retailers now require:

- multi-payment support

- real-time transaction processing

- reliable uptime

- integrated reporting

With Unipesa, retail businesses can:

- process multiple payment types through a unified system

- reduce payment friction

- improve transaction reliability

Result: Faster checkout experiences and more efficient payment operations.

Agent Banking Networks

One of the most powerful applications of POS systems is agent banking.

Agents use POS devices to provide:

- cash withdrawals

- deposits

- transfers

- payment services

This extends financial services into:

- underserved areas

- remote communities

- cash-dominant environments

Key insight:

POS systems become physical access points to digital finance.

Cash-In and Cash-Out Operations

Cash remains essential in many markets.

POS systems bridge:

- physical cash

- digital financial systems

Through POS-enabled agents, users can:

- convert cash into digital balances

- withdraw digital funds as cash

This creates:

- financial accessibility

- liquidity access

- broader participation in digital economies

Bill Payments and Utility Services

POS systems increasingly support:

- utility bill payments

- airtime top-ups

- subscription services

Benefits include:

- convenience for users

- additional revenue streams for agents and merchants

- increased transaction volume

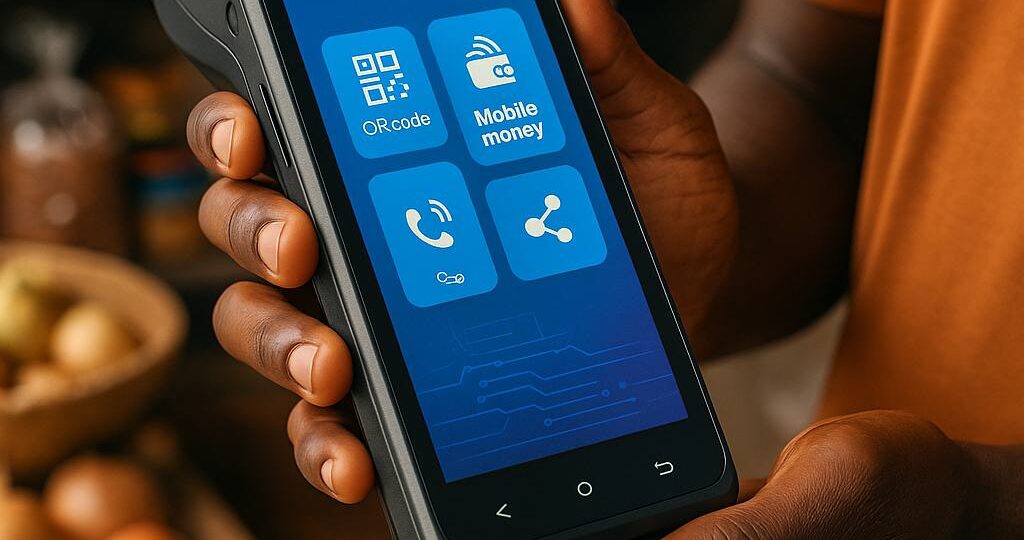

Wallet and Mobile Money Integration

Modern POS systems must support:

- digital wallets

- mobile-based payments

- QR-based transactions

Unipesa enables this through:

- multi-rail payment connectivity

- unified infrastructure access

- seamless transaction orchestration

Result: One POS system can support multiple financial ecosystems simultaneously.

SME Financial Services

POS systems are also becoming data and service hubs for SMEs.

They can support:

- transaction analytics

- repayment collection

- credit-linked services

Transaction activity creates valuable insights into:

- business performance

- cash flow behavior

- operational consistency

This enables future financial services such as:

- embedded lending

- working capital access

- data-driven financial products

Multi-Market Scalability

Scaling POS systems across markets is complex.

Each market introduces:

- different payment providers

- different regulations

- different transaction behaviors

Infrastructure platforms simplify this challenge.

Unipesa enables:

- centralized integration

- unified transaction management

- scalable deployment across markets

Reliability Across Use Cases

Versatility is meaningless without reliability.

POS systems must operate consistently across:

- high-volume retail environments

- distributed agent networks

- unstable connectivity conditions

This requires:

- smart routing

- failover systems

- continuous monitoring

Unipesa supports this through:

- real-time infrastructure optimization

- transaction monitoring

- multi-provider connectivity

Security Across Financial Operations

Because POS systems handle:

- payments

- identity verification

- financial activity

Security becomes critical.

Core requirements include:

- encrypted transaction flows

- secure authentication

- fraud prevention mechanisms

Infrastructure-level security ensures trust across every use case.

The Shift Toward Intelligent POS Infrastructure

Modern POS systems are evolving into:

- connected financial nodes

- intelligent transaction layers

- operational data hubs

Future capabilities may include:

- AI-driven transaction routing

- predictive analytics

- automated optimization

The Business Impact of Versatile POS Systems

For businesses and operators, versatile POS infrastructure creates:

1. Expanded Revenue Opportunities

More transaction types → more monetization paths

2. Greater Customer Reach

Ability to serve multiple customer segments

3. Improved Operational Efficiency

Unified systems reduce complexity

4. Better Scalability

Infrastructure-driven deployment across markets

Conclusion: POS Infrastructure as a Financial Ecosystem Layer

POS systems are no longer just devices.

They are: multi-purpose infrastructure layers powering modern financial ecosystems

From:

- retail shops

- to agent banking networks

- to digital financial services

their role continues to expand.

Platforms like Unipesa make this evolution possible by enabling:

- connectivity

- scalability

- reliability across use cases

Because in modern fintech:

The most valuable POS systems are not those that process transactions.

They are those that connect entire financial ecosystems.