Blockchain and Fintech: Beyond Cryptocurrency in Africa

Introduction: The Wrong Narrative About Blockchain

For years, blockchain in Africa has been framed as a story about cryptocurrency adoption.

That narrative is incomplete.

Across the continent, the real transformation is happening quietly — not in trading apps, but in financial infrastructure. Blockchain is increasingly being used to improve how money moves, how identity is verified, and how systems connect.

And nowhere is this shift more visible than in fintech.

Africa Already Has Strong Payment Systems, But They Don’t Connect

Africa is not lacking financial innovation. In fact, it has some of the most advanced local payment ecosystems in the world.

Platforms like M-Pesa in East Africa and Mazzuma in Ghana have transformed how millions of people transact daily.

They have:

- Built massive user bases

- Enabled mobile-first payments

- Created local financial ecosystems

But they also highlight a more profound issue:

Each system is powerful locally but disconnected globally.

For fintech companies trying to scale across Africa, this situation creates a structural challenge:

- Every market requires new integrations

- Every system operates differently

- Cross-border transactions remain complex

This is where the next layer of innovation begins.

Blockchain Is Not Replacing These Systems — It’s Connecting Them

The most successful blockchain implementations in Africa are not trying to replace mobile money or banks.

Instead, they are being used to:

- Improve settlement speed

- Reduce cross-border friction

- Enable interoperability

For example:

- Cross-border transactions can be optimized using blockchain-based settlement layers

- Stablecoin infrastructure can reduce FX inefficiencies

- Transaction transparency can improve trust and compliance

But this only works when blockchain is integrated into existing financial rails, not built in isolation.

The Rise of Hybrid Infrastructure

What is emerging is not a “blockchain-first” ecosystem but a hybrid financial infrastructure.

In this model:

- Mobile money systems like M-Pesa remain critical

- Local platforms like Mazzuma continue to dominate their markets

- Banks and card networks still play a role

Blockchain becomes:

A coordination layer, not a replacement layer

However, integrating all of these systems across multiple countries is not trivial.

The Real Bottleneck: Integration at Scale

For fintech companies, the greatest challenge is not access to technology — it’s integration complexity.

To scale across Africa, a business often needs to:

- Connect to mobile money systems in multiple countries

- Integrate with banks and card processors

- Navigate regulatory requirements

- Handle cross-border settlement

Doing this manually is slow, expensive, and difficult to scale.

Where Infrastructure Platforms Change the Game

This is where platforms like Unipesa become critical.

Instead of integrating each system individually, businesses can:

- Access multiple payment methods through a single API

- Connect to mobile money, banks, and cards across markets

- Build cross-border capabilities without rebuilding infrastructure

In this model:

- M-Pesa and Mazzuma remain essential local systems

- Blockchain enhances settlement and coordination

- Unipesa provides the unifying infrastructure layer

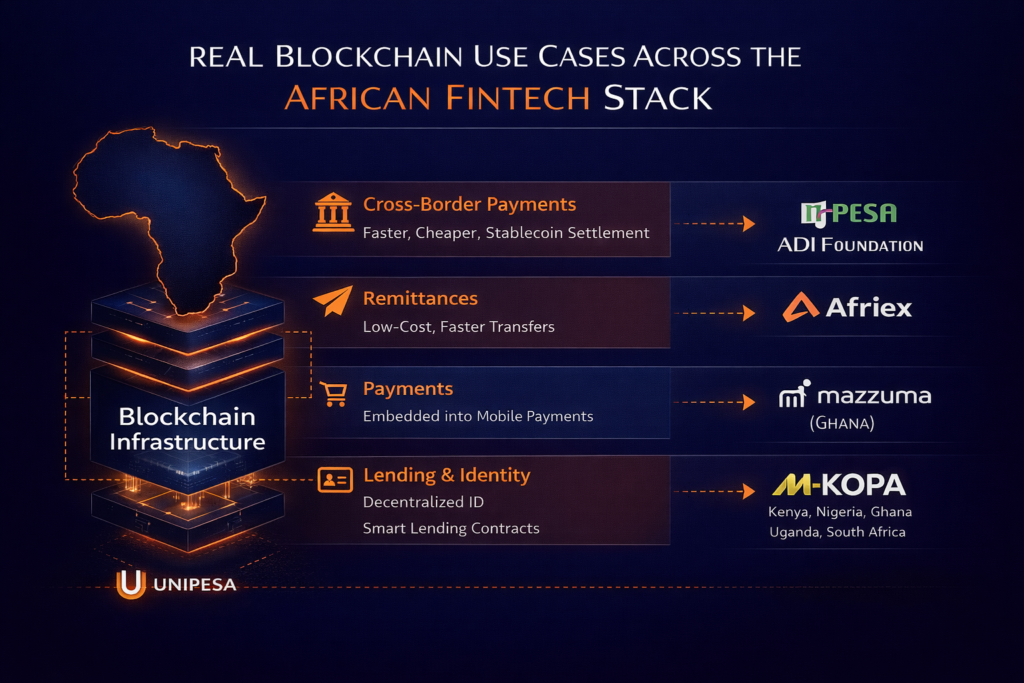

Real Use Cases: Where Blockchain Actually Adds Value

1. Cross-Border Payments

- Faster settlement using blockchain layers

- Reduced reliance on correspondent banking

- Lower transaction costs

2. Remittances

- More efficient money transfers into African markets

- Improved liquidity and routing

3. Identity and Compliance

- Portable KYC systems

- Reduced onboarding friction

- Better fraud prevention

4. Lending and Credit Infrastructure

- Transparent credit histories

- Automated loan execution via smart contracts

Why “Blockchain-Only” Models Don’t Scale

Many blockchain startups fail in Africa because they:

- Ignore local payment behavior

- Don’t integrate with existing systems

- Underestimate regulatory complexity

The result:

- Low adoption

- Poor user experience

- Limited scalability

The winning model is different:

Infrastructure-first, with blockchain embedded where it adds value.

The Future: Invisible Blockchain, Connected Systems

Standalone blockchain platforms will not define the next phase of fintech in Africa.

It will be defined by:

- Seamless payment experiences

- Cross-border interoperability

- Infrastructure that abstracts complexity

Users won’t care whether blockchain is used.

They will care about:

- Speed

- Cost

- Reliability

And that requires a combination of:

- Strong local systems (like M-Pesa, Mazzuma)

- Emerging technologies (like blockchain)

- Unified infrastructure platforms (like Unipesa)

Conclusion: From Fragmentation to Infrastructure

Africa’s fintech ecosystem is not being rebuilt — it is being connected.

Blockchain plays a role in this transformation, but not as a replacement for existing systems.

Its real value lies in:

- Enhancing interoperability

- Improving efficiency

- Enabling new financial models

The companies that will lead this transformation are not those building isolated technologies but those creating infrastructure that connects everything.