Payment Infrastructure vs Payment Gateway: What’s the Difference?

As digital commerce expands across Africa and other emerging markets, the payments ecosystem is becoming more complex. Businesses now accept payments through multiple channels, including cards, mobile money, bank transfers, digital wallets, and POS networks.

Many companies entering the fintech space encounter two common terms: payment gateway and payment infrastructure. Despite their relatedness, these concepts represent distinct layers within the digital payments ecosystem.

Understanding the difference between payment gateways and payment infrastructure is essential for fintech startups, banks, marketplaces, and merchants that want to build scalable financial services.

This article explains how both systems work, how they differ, and why modern fintech platforms increasingly rely on infrastructure rather than standalone gateways.

What Is a Payment Gateway?

A payment gateway is a technology that enables merchants to accept digital payments by connecting their website, app, or POS system to a payment processor.

In simple terms, a payment gateway acts as a bridge between a merchant and the financial institutions involved in processing a payment.

When a customer makes a payment online or through a terminal, the payment gateway performs several functions:

- securely collects payment details

- encrypts sensitive data

- sends the transaction to the payment processor

- communicates with banks or card networks

- returns the authorization result

For example, when a customer pays with a card on an e-commerce website, the payment gateway transmits the card information to the processor and waits for approval from the issuing bank.

If the payment is authorized, the transaction is completed.

Payment gateways have long been a fundamental component of digital commerce.

The Limitations of Payment Gateways

While payment gateways are useful for accepting payments, they typically focus on a single function: processing transactions through a specific provider or network.

This creates several limitations for businesses operating at scale.

First, most gateways rely on a single payment provider or processor, which means merchants depend on that provider’s performance and availability.

Second, gateways generally do not manage multiple payment systems simultaneously. Businesses that need to integrate with additional providers often must implement separate integrations.

Third, gateways typically provide limited capabilities for managing payment routing, optimization, or infrastructure-level control.

For small merchants, these limitations may not be significant. However, fintech platforms and companies operating across multiple markets often require a more flexible infrastructure layer.

What Is Payment Infrastructure?

Payment infrastructure refers to the underlying systems that enable digital payments to operate at scale across multiple providers, networks, and financial institutions.

Rather than serving as a single connection point like a gateway, payment infrastructure acts as a comprehensive platform that manages the entire payment ecosystem.

Payment infrastructure typically includes components such as:

- payment orchestration

- wallet systems

- transaction routing

- settlement management

- fraud detection

- compliance tools

- reporting and analytics

This infrastructure allows companies to connect to multiple payment providers, manage transactions across different channels, and optimize payment performance.

In other words, payment infrastructure provides the foundation on which payment systems operate.

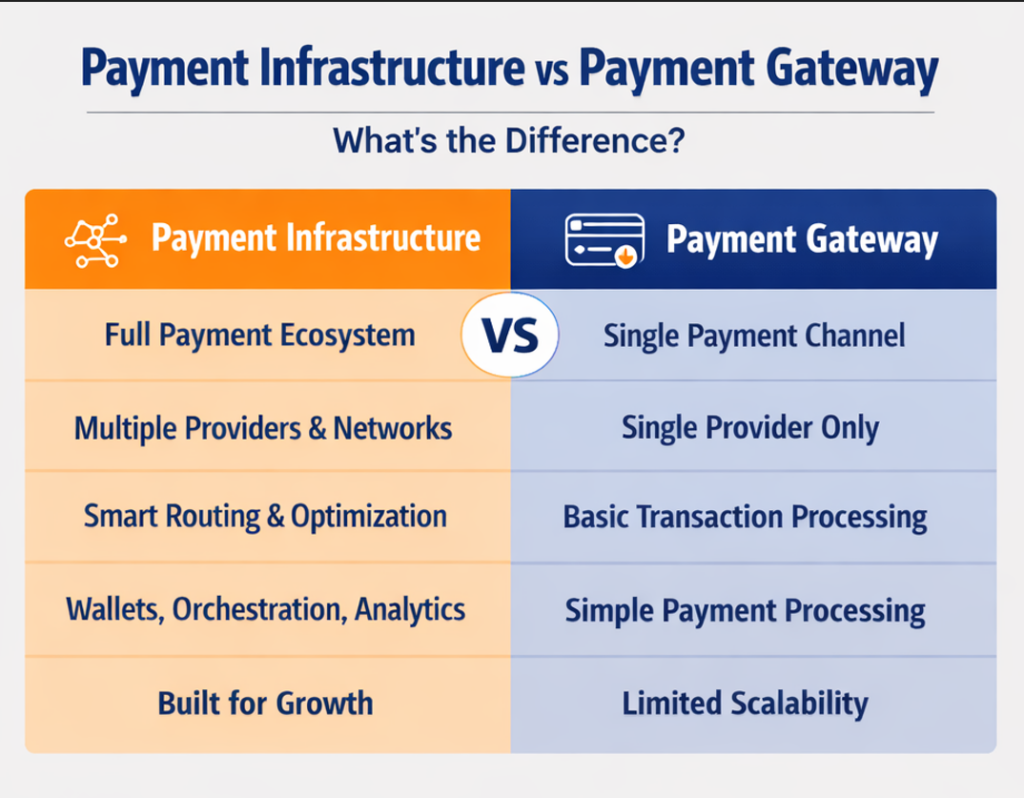

Key Differences Between Payment Gateways and Payment Infrastructure

The difference between a payment gateway and a payment infrastructure becomes clearer when comparing their capabilities.

| Feature | Payment Gateway | Payment Infrastructure |

| Purpose | Process payments | Manage the full payment ecosystem |

| Integrations | Usually one provider | Multiple providers and networks |

| Routing | Limited | Smart routing across providers |

| Scalability | Moderate | Built for large-scale platforms |

| Payment optimization | Minimal | Advanced optimization tools |

| Infrastructure layer | Surface-level | Core infrastructure |

A payment gateway is a tool for accepting payments, while a payment infrastructure is a platform for managing payment ecosystems.

Why Fintech Platforms Need Payment Infrastructure

Modern fintech platforms rarely operate in a single payment environment.

They often need to support multiple payment channels such as:

- mobile money

- bank transfers

- card payments

- POS transactions

- digital wallets

Each payment channel may involve different financial institutions and technical integrations.

Without a unified infrastructure layer, managing these systems can quickly become complicated.

Payment infrastructure platforms simplify this process by providing centralized tools that manage all payment channels through a single system.

This allows fintech companies to expand their services while maintaining operational efficiency.

Payment Infrastructure in African Fintech

Africa’s payment ecosystem is particularly diverse.

Different countries rely on different payment methods, including

- mobile money networks

- bank transfers

- card payments

- agent networks

- digital wallets

This diversity creates challenges for companies building fintech platforms that operate across multiple markets.

Payment infrastructure platforms help solve this problem by integrating multiple payment rails within a unified system.

Infrastructure providers enable fintech companies to connect to various payment methods without building separate integrations for each provider.

Beyond Payments: Infrastructure for Financial Platforms

Another major advantage of payment infrastructure is that it supports more than just payment processing.

Many infrastructure platforms also provide additional financial services, including:

- digital wallet systems

- POS network management

- lending platforms

- transaction analytics

- compliance monitoring

This allows fintech companies to build comprehensive financial ecosystems rather than standalone payment products.

For example, a fintech platform may combine payment processing with wallet services, merchant tools, and lending products to create a full financial solution.

Such ecosystems are difficult to build using only payment gateway technology.

Infrastructure Platforms and Fintech Innovation

Across the global fintech industry, infrastructure platforms are becoming increasingly important.

Instead of building complex financial systems internally, many fintech startups now rely on specialized infrastructure providers that offer ready-to-use financial technology.

These infrastructure platforms enable companies to launch financial products faster while reducing development costs.

Companies like Unipesa provide financial infrastructure designed for fintech platforms operating across African markets.

Through integrated payment systems, wallet infrastructure, and POS networks, fintech companies can deploy scalable financial services without building each component from scratch.

The Future of Payment Systems

As digital commerce continues to grow, the role of payment infrastructure will become even more significant.

Businesses increasingly require payment systems that are:

- scalable

- flexible

- multi-provider

- optimized for performance

Payment gateways will continue to play an important role in processing individual transactions. However, infrastructure platforms are becoming the backbone of modern fintech ecosystems.

Companies that rely solely on gateway-based systems may face limitations as their payment operations expand.

In contrast, platforms built on strong infrastructure can adapt to new payment methods, markets, and technologies.

Final Thoughts

Payment gateways and payment infrastructure serve different but complementary roles within the digital payments ecosystem.

Payment gateways enable merchants to accept payments, while payment infrastructure provides the systems needed to manage payments at scale.

For fintech companies operating in dynamic markets such as Africa, infrastructure platforms offer the flexibility and scalability needed to support diverse payment methods and expanding financial ecosystems.

As fintech continues to evolve, payment infrastructure will play an increasingly central role in enabling the next generation of digital financial services.